Why the Iran War Changed Uranium's Timeline

Here's what the conflict in the Middle East means for the future of nuclear energy and the uranium supply chain going forward.

As the fallout from the U.S.-Israel war on Iran continues to compound, a key component of the global energy story is coming into focus and it is not oil. It is the uranium supply chain that the war has suddenly thrown back into view.

That supply chain has been under strain since Russia invaded Ukraine in February 2022. Within weeks of that invasion, it was obvious that Western utilities had built their nuclear fuel supply chains around a country that was now at war with NATO allies. That risk was fortified by the fact that Rosatom, Russia’s state nuclear corporation, controls 40-45% of global uranium enrichment capacity. Kazakhstan, which is closely aligned with Moscow, is the world’s largest uranium producer.

Those contracts with Russia had made sense for years. Russian enrichment was cheap and reliable. The reality was that few Western government officials wanted to look too hard at the risk. The broad sanctions that followed the invasion made uranium dependency hard to ignore publicly, even if nothing changed in practice, in the immediate aftermath.

U.S. utilities kept paying Tenex, Rosatom’s trading arm, more than $1 billion a year for enrichment services. That kept flowing even as the U.S. government sanctioned Russian banks, energy companies, and state officials. Two years of pressure from domestic producers and national security advocates eventually got a bill through Congress.

The Prohibiting Russian Uranium Imports Act was passed in May 2024. But it included waivers allowing utilities to keep buying Russian fuel through 2028, because there was nowhere else to get it. Russia responded with its own export ban in November 2024. Enriched uranium deliveries resumed in early 2025 after both sides negotiated one-off licenses. Yet, though the ban is technically in effect, U.S. dependency has not been removed.

What the Iran War Revealed

Now, to be clear, Iran didn’t supply enriched uranium to Western utilities. And it is not part of the supply chain that we’re focused on. But the fact that Iran’s nuclear enrichment facilities are back in the crosshairs of geopolitics and energy policy matters to how governments consider their nuclear power strategy.

In June 2025, the U.S. and Israel struck Iran’s three main nuclear sites. Natanz and Fordow are underground enrichment facilities where Iran was producing enriched uranium. Isfahan is the conversion plant that feeds them. The White House declared Iran’s nuclear program destroyed.

By February 2026 U.S. intelligence and satellite imagery were alleging a different picture. Iran had spent those months hardening and dispersing what remained, moving centrifuge equipment to deeper, harder-to-reach facilities and beginning active reconstruction. The program the White House declared obliterated was claimed to have been rebuilt within eight months.

Iran didn’t abandon its nuclear strategy because the U.S. bombed the facilities. The U.S.-Russia enrichment relationship has the same modus operandi. Russia has decided that its position in the global fuel cycle is strategic. The Russian uranium ban that passed in Washington in 2024 does not change that math. For the U.S. and Western allies, the only exit is building domestic capacity that makes the Russian supply unnecessary.

Passing the ban did not solve the underlying problem, which is a lack of sufficient domestic or allied-provided enrichment capacity. Both sides have been issuing one-off licenses to keep deliveries moving, as neither can afford a clean break before 2028. The U.S. runs more nuclear reactors than any other country. It also still buys the fuel it needs from Russia.

The Supply Deficit Existed Before February 28

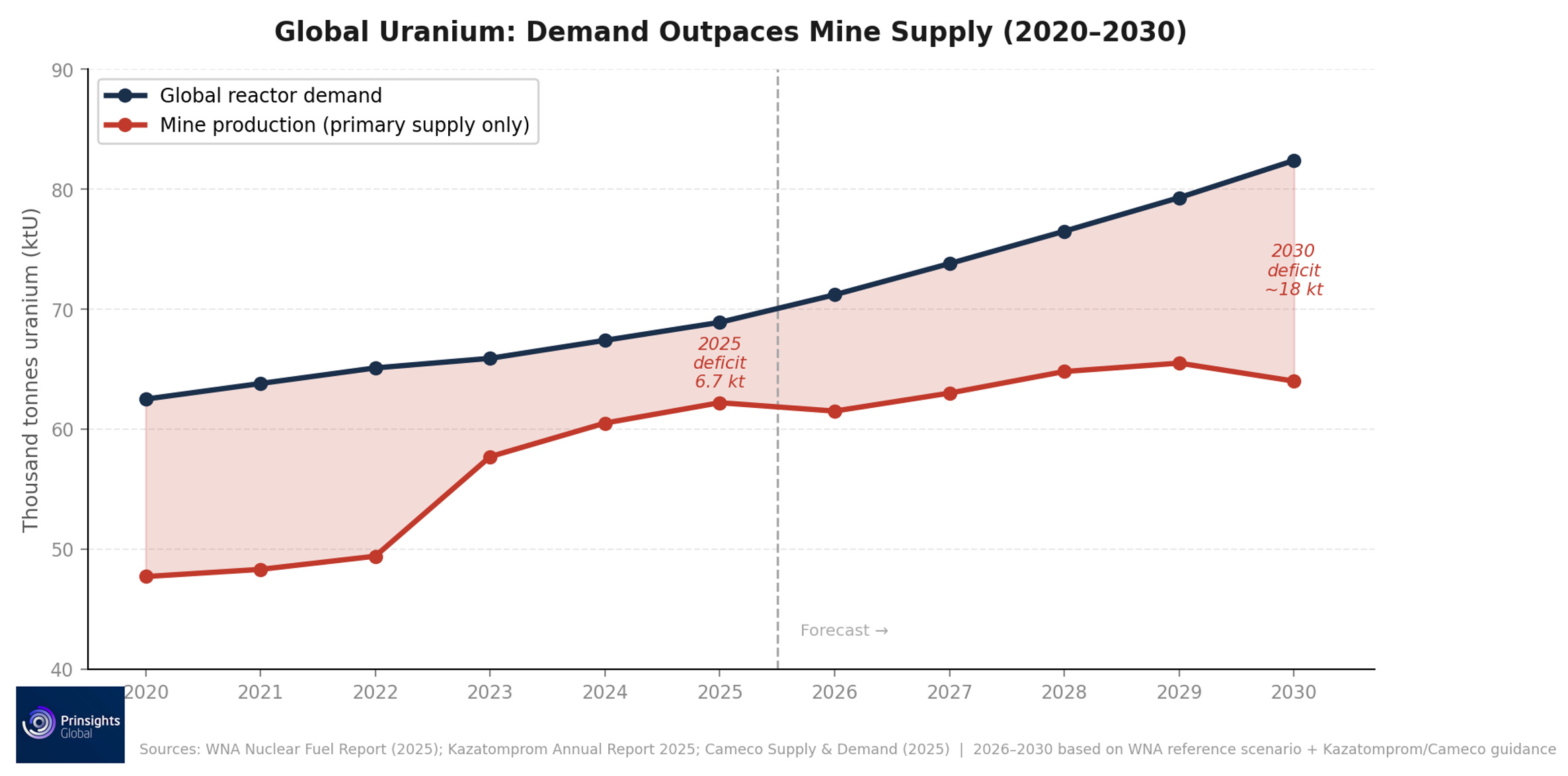

Global reactor demand outpaced mine supply in 2025, with 68.9 kilotonnes consumed vs. 62.2 kilotonnes produced. Countries are now rushing to sign long-term contracts to lock up what’s available for periods up to a decade moving forward. The chart below shows why the gap will not close on its own. Existing mines are approaching production limits.

The two largest new projects in the pipeline are Denison’s Phoenix ISR mine in Saskatchewan, which is targeting first production in mid-2028 pending final regulatory approval, and NexGen’s Rook I, which just received its construction licence and is expected to come online around 2030. Neither project would come near to closing the U.S. or global supply-demand gap.

On March 2, India entered a nine-year deal with Canada’s Cameco for 22 million pounds of uranium, with deliveries running from 2027 through 2035. The contract is valued at roughly $1.9 billion at current prices.

Several weeks before that, in February, Kazakhstan’s Kazatomprom announced a separate large supply agreement with India, pending shareholder approval expected in April. India currently operates 24 reactors, with plans to scale to 100 gigawatts of nuclear capacity by 2047.

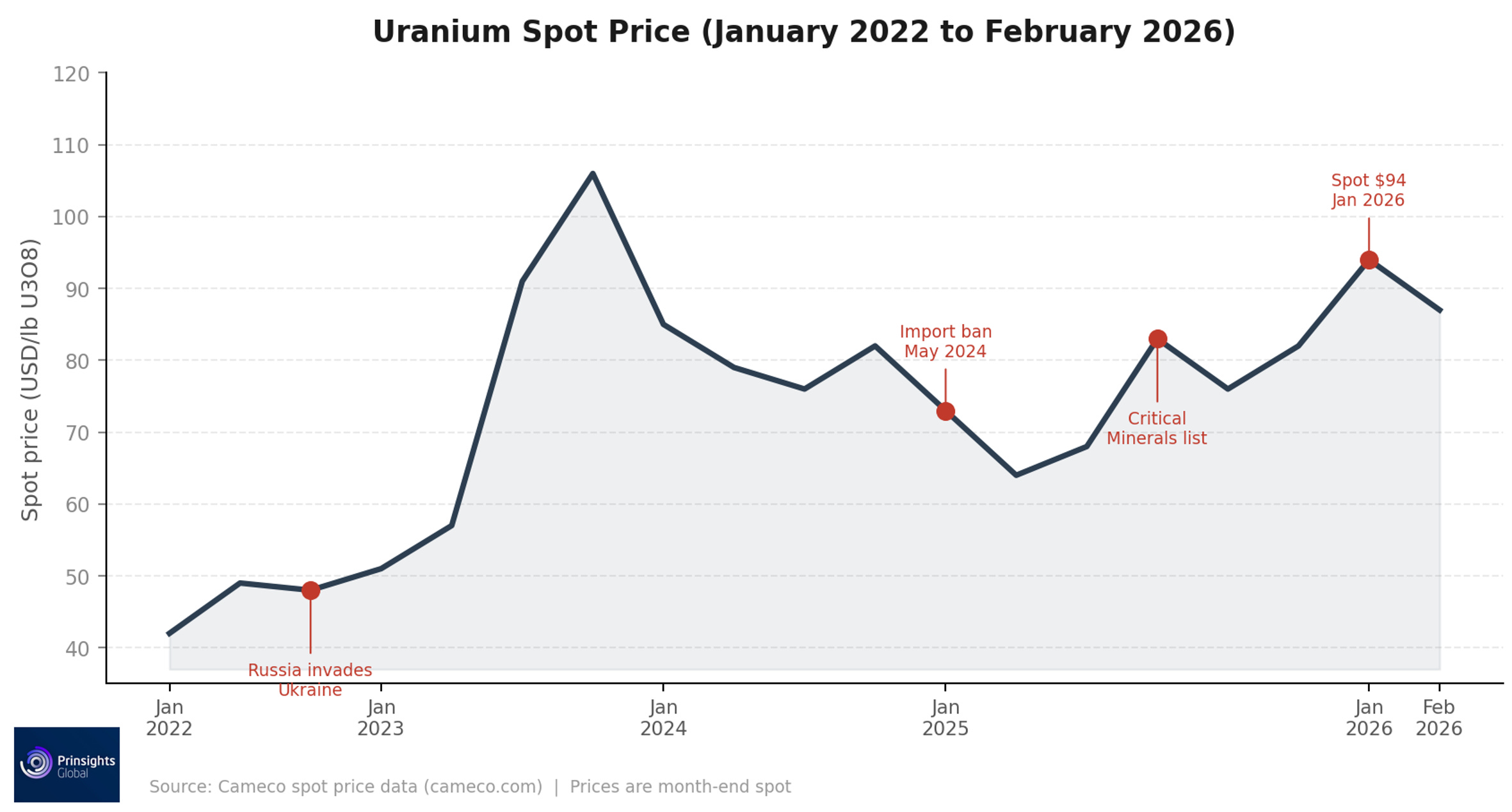

Such strategic future supply lockdown moves don’t filter into spot prices immediately because there’s no main uranium exchange-traded product – but they will. Uranium spot prices hit $94 at the end of January and briefly touched $101 in futures before pulling back to $86.95 at the end of February. But with contracts like those India just scored that are working to lock up future supply, we expect spot prices and forward contracting prices to rise.

Going into 2026, U.S. utilities had promised more uranium to their reactors than they had contracted to buy. That gap is roughly 34 million pounds through the 2030s.

In addition, despite a surge in 2024 and 2025, domestic uranium production remains depressed after years of low prices and mine closures, covering roughly 2-3% of the approximately 50 million pounds loaded into U.S. reactors in 2024. The U.S. still relies on imports for 99% of the uranium it uses in power plants.

That means that even if mining output recovers, raw uranium still has to be enriched before it can go into a reactor. And the only commercial-scale enrichment facility operating in the U.S. is Urenco USA in New Mexico, which is European-owned and supplies about a third of domestic needs.

Meanwhile, the January 2028 deadline for ending Russian imports is less than two years away. The facilities that would close that gap have not been built. And this conflict should serve as another wake-up call to speed up the process.

Washington Has Started the Framework. The Supply Chain Must Catch Up

Since the oil shocks of the 1970s, the West has spent more than fifty years diversifying its oil supply chain. Yet the uranium supply chain never went through that same reckoning. It is going through one now. But the “catch up” phase will take years, not months.

The timeline:

In May 2025, Trump signed executive orders directing the Nuclear Regulatory Commission (NRC) to cut reactor licensing timelines and directing the U.S. Department of Energy (DOE) to develop a domestic spent fuel recycling policy.

In October 2025, the White House committed to financing and permitting a fleet of Westinghouse AP1000 reactors as part of an $80 billion strategic partnership with Westinghouse’s owners, Cameco and Brookfield.

In November 2025, uranium was then reinstated to the U.S. Geological Survey (USGS) Critical Minerals List.

Then, in January 2026, the DOE awarded $2.7 billion in enrichment contracts to three domestic producers. That is a policy framework that requires a functioning and expanding supply chain.

All of these indicators signal that momentum is not just pushing the sector forward, but that policy and the private sector are aligning more rapidly – and that’s where investment opportunities are emerging.

That’s why our Founders+ monthly issue for March, out tomorrow, is focusing on a domestic uranium company in the U.S. that most people don’t know about, yet it sits inside the expansion policy pipeline, directly in the path of everything we just described.

Not a Founders+ member? This is a great moment to join our highest tier. The recommendation and research-backed analysis is only available for those subscribed. We can’t wait to share the issue with you.

You can upgrade here now.

How do Breeder reactors figure into this? It would seem that may be an offset to supply chain dependency.

Hi I am a founders member already! Can you please change!!!