Unpacking the U.S. Steel Deal

Unpacking the U.S. Steel Deal

As the Nippon Steel and U.S. Steel merger deal appears to be faltering, here's what it could mean for infrastructure, merger trends and the geopolitical landscape.

The world of mergers and acquisitions faced a finance-meets-politics battle.

In a hyper-polarized election, both presidential candidates landed on the same side of the fight.

They don't want Japanese steel giant, Nippon Steel Corporation to buy U.S. Steel.

Beyond political motivations, the proposed deal raises questions about the state and future of United States manufacturing industry and infrastructure.

It gets complicated – and easy from there.

Let’s unpack the proposed deal and what it signals.

A Brief History of U.S. Steel

On February 5, 1901, famed American moguls Andrew Carnegie, J.P. Morgan, Charles Schwab and Elbert H. Gary, U. S. Steel's first chairman, formed U.S. Steel by merging several steel companies.

During its first year, the company produced 67% of all steel in America.

U.S. Steel played an integral part in U.S. history. The firm supplied steel for iconic American buildings, bridges, and other structures.

Stretching from the iconic San Francisco-Oakland Bay Bridge to the Willis Tower in Chicago, the imprint that U.S. Steel made is still apparent today.

Known as “The Corporation,” it was once considered the largest company in the world and the first to top more than $1 billion in U.S. history.

But over time, things have changed. Steel was once used for sweeping infrastructure and major projects ranging from massive skyscrapers to ships and rail tracks.

And while infrastructure is seeing a renewed focus, the booming demand for new skyscrapers and Titanic-like ships is not what it was at the start of the 1900’s, or even through much of the last century.

In 2014, U.S. Steel lost its spot in the S&P 500. Today, it’s only the third-biggest steel producer in the country. Globally, U.S. Steel is the 24th-largest steel company, according to data from the World Steel Association.

Enter Nippon Steel Corporation (NSC). The Tokyo-based company was established in 1970, through a merger. It is the world's fourth-largest steel producer and the largest in Japan.

In today's cross-border mergers and acquisitions (M&A) environment, the deal makes perfect sense.

However, in an election year and for a company that’s headquartered in a crucial swing state that both candidates want to win, politics entered into the mix.

The Corporate Benefits

The Nippon Steel – U.S. Steel merger would have created the world’s third largest steel producer.

Nippon Steel Corporation operations span the Americas, Europe, and Asia. It’s renowned for high-quality products, engineering and advanced technology. U.S. Steel primarily operates across North America, Europe, and Asia.

One main reason for U.S. Steel's decision to sell itself to Nippon Steel is market diversification. By partnering with a Japanese steel goliath, the firm can access a larger global customer base and a wider range of steel products and resources.

On the other hand, Nippon Steel Corporation could benefit from leveraging U.S. Steel's strong brand reputation. But it goes beyond that.

U.S. Steel offers Japan and the U.S. a chance to push for equilibrium against geopolitical rivals like China. Nippon Steel’s executive vice president claimed that the deal would make them “better equipped to compete with the Chinese behemoths that dominate the industry.

The move would strengthen alliances between these major import and export partners.

By pooling resources, technology, and expertise the two firms could streamline operations and reduce overhead. This could not only enhance profitability – but do so in an increasingly competitive market.

Click here now to upgrade and unlock exclusive Premium Prinsights!

The Deal and the Fight

Here’s a brief recap of the details. Nippon Steel Corporation made an offer to buy U.S. Steel for $14.9 billion in December, 2023, in an all-cash deal for $55 per share. That was a 40% premium over the prevailing share price.

Under the terms, U.S. Steel could keep its iconic name and even its headquarters in Pittsburgh, Pennsylvania.

However, the United Steelworkers union opposed the deal after being left out at the start and on fears it will lead to layoffs and plant closings.

President Biden came out against the deal as well. Former president Donald Trump reflected that he, too, would block the deal.

Vice President Kamala Harris, while campaigning with President Biden in Pennsylvania, also said she opposed the U.S. Steel deal.

Nippon Steel promised not to lay off workers or close plants. However, the union argued that its proposal contains too many loopholes that allow Nippon to back out.

While the workers concerns are valid, the truth is that if the two companies are able to come to the table with terms that meet the workers’ concerns, the national security argument against this deal might hold less weight.

Whatever the deal’s outcome, there are broader key themes that it highlights.

Three Factors Impacting the Trend Pushing for a Steel Merger

The potential sale of U.S. Steel to Nippon Steel reflects broader global consolidation trends.

1 – Mergers are Rebounding

According to The World Steel Association, next year’s forecasts show a projected 1.2% total increase in mergers globally. Before the world shut down from Covid in 2020, global M&A in the steel industry from 2015 to 2019 totaled an estimated $47 billion. The steel industry will likely experience continued growth from global demand for finished steel products led by Asia. That could entail more mergers.

On the other hand, the U.S. will continue to have less comparative demand for steel until it elevates and prioritizes investment in domestic infrastructure – or it works to create a national infrastructure bank to finance such projects.

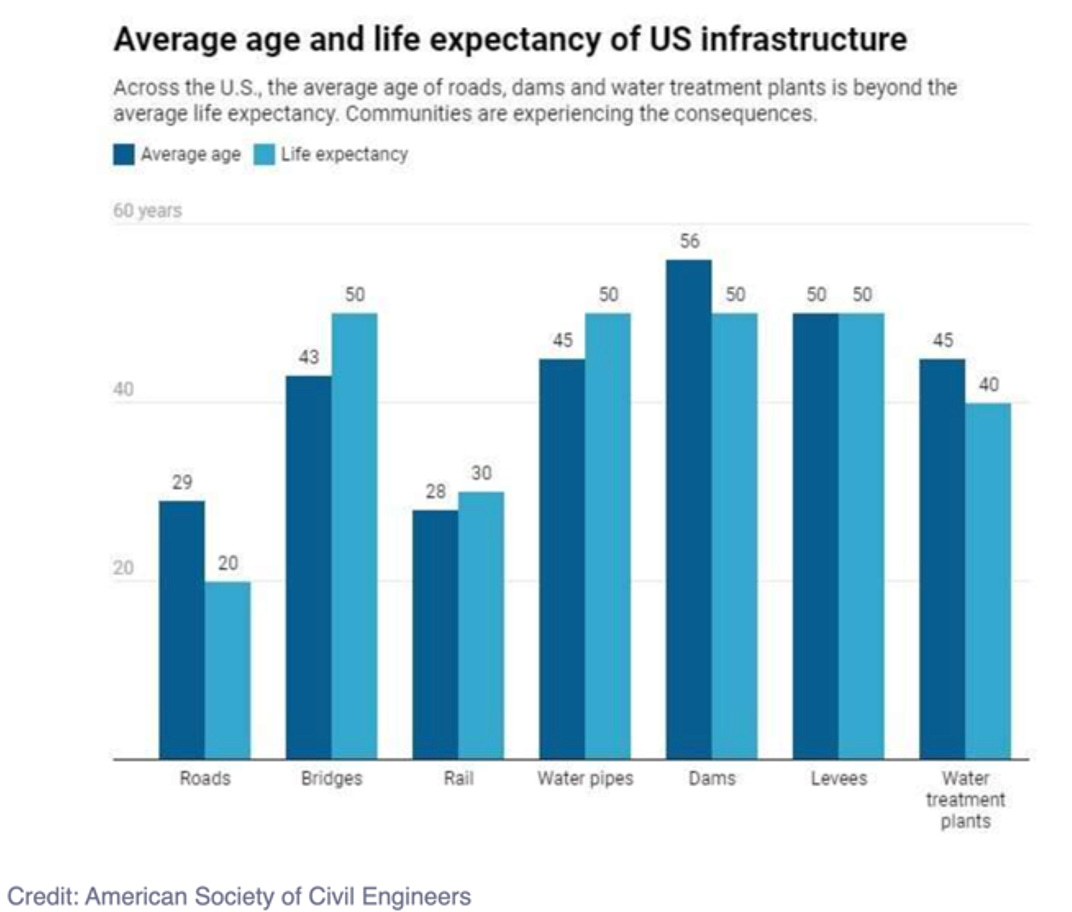

2 – Infrastructure is a Critical Need

Every four years, the American Society of Civil Engineers assesses the nation’s 17 major infrastructure categories. They gave the U.S. a C- in their 2021 U.S. infrastructure report card.

That’s because, among other infrastructure shortfalls, 42% of U.S. bridges (one of the 17 categories) are more than 50 years old. Almost 400,000 were built between 1950 and the turn of the 21st century. And over 46,000 are structurally deficient or in “poor” condition.

These figures should not only raise alarm bells about our infrastructure needs – but signal the future and critical role that steel will have to play in the U.S. if they are addressed.

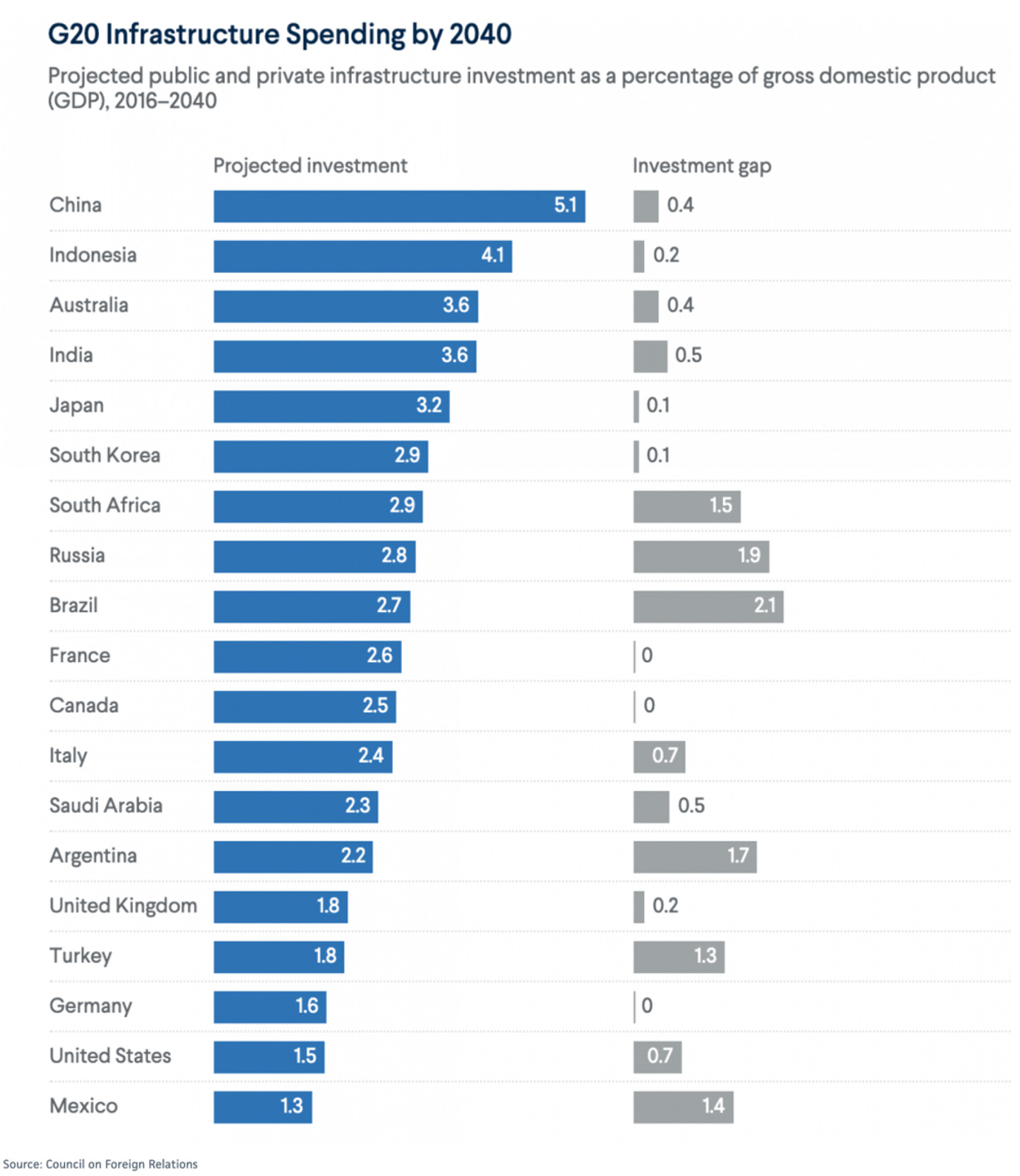

Compared to other major countries, U.S. investment in infrastructure as a percent of GDP is projected to remain at an embarrassingly low position over the next decade and a half.

That’s one reason that foreign direct investment (FDI) in the U.S. grew by over $227 billion in 2023. The FDI in the manufacturing industry increased by the most, going from $58.6 billion to a total investment of $2.22 trillion.

3 – A Weaker Dollar Will Drive More Foreign Investment

What you should know is that the weaker the U.S. dollar becomes, the more that trend will accelerate. As the Federal Reserve cuts interest rates, this should only further that pattern.

As we saw in 2023, Europe, Asia and Canada are looking to invest more in the U.S. If the cost of doing business, heavily influenced by the U.S. dollar, becomes more favorable, then the expectation is that even more international interest will be attracted to U.S. outlets.

What the Deal Means

In general, if both companies' boards and shareholders approve, this deal should go through as it would for any other similar-sized firms. But, as elections and politics blur the lines that may not be the case.

This week, Nippon Steel’s vice-chair met with senior U.S. officials for high-level discussions on the $15 billion deal. The Committee on Foreign Investment in the U.S. reportedly concluded that the deal could pose security risks to the U.S. However, other government agencies including the Pentagon to the U.S. State Department were reported to not be aligned with that conclusion.

Regardless of where this deal lands, the future of U.S. infrastructure, jobs and capital hangs in the balance. So could the fate of commodity prices, related mergers, and dollar-dependent foreign investment in U.S. manufacturing.

Overall, infrastructure, steel production and M&A trends are expected to see a considerable boost after the November elections. One way to tap into this trend and the growing global steel demand is to consider the SPDR S&P Metals and Mining ETF (XME). It provides exposure to publicly traded companies involved in steel production.

I paid for a subscription and have a receipt, so why am I not getting paid content.