Politics, Power and Another Fed Misstep

Politics, Power and Another Fed Misstep

While the Fed's historic rate cuts get headlines, the central bank's move to weaken safeguards for Wall Street banks should be the real concern for the financial system. Here's why...

Since 2020, the Federal Reserve and its monetary policy defined a mini-era of monetary policy, investing and finance. At 2 pm ET that period begins to come to an end for the U.S. economy – and the world.

What transpired is that inflation hit highs not seen in four decades, peaking in 2022 and continuing to linger even today.

Federal Reserve chairman Jerome Powell’s ability to deliver an aggressive hiking cycle and then maintain rates for an extended period in response, without a recession (so far), defies logic. Something had to break first.

Now, as weaker job numbers emerge, the Fed is backing away from the brink of pushing the economy too close to disaster – even with inflation above its target.

What appears to be gone (at the moment) are the days of record-low mortgage interest rates and other accessible lines of credit for things like buying cars and starting businesses.

Only now, elections, policies and weakened safeguards are being factored into a new era.

Elections and Changing Monetary Policy

To be clear, the elections are not the Fed’s domain. Yes, the leadership there is filled with political appointees, selected by presidents and confirmed by Congress. But the institution, for the most part, is legally consigned to focus on the monetary system and not political discourse.

And while the Fed’s policy shift before a major presidential election can be seen as political – it’s not in the way you might think. You see, by the Fed reversing course on interest rates, it is admitting that something is concerning in the economy – or even the financial system.

The incumbent Democratic party might be quick to highlight areas of the economy that show progress – but the Fed is not cutting rates because the economy is booming.

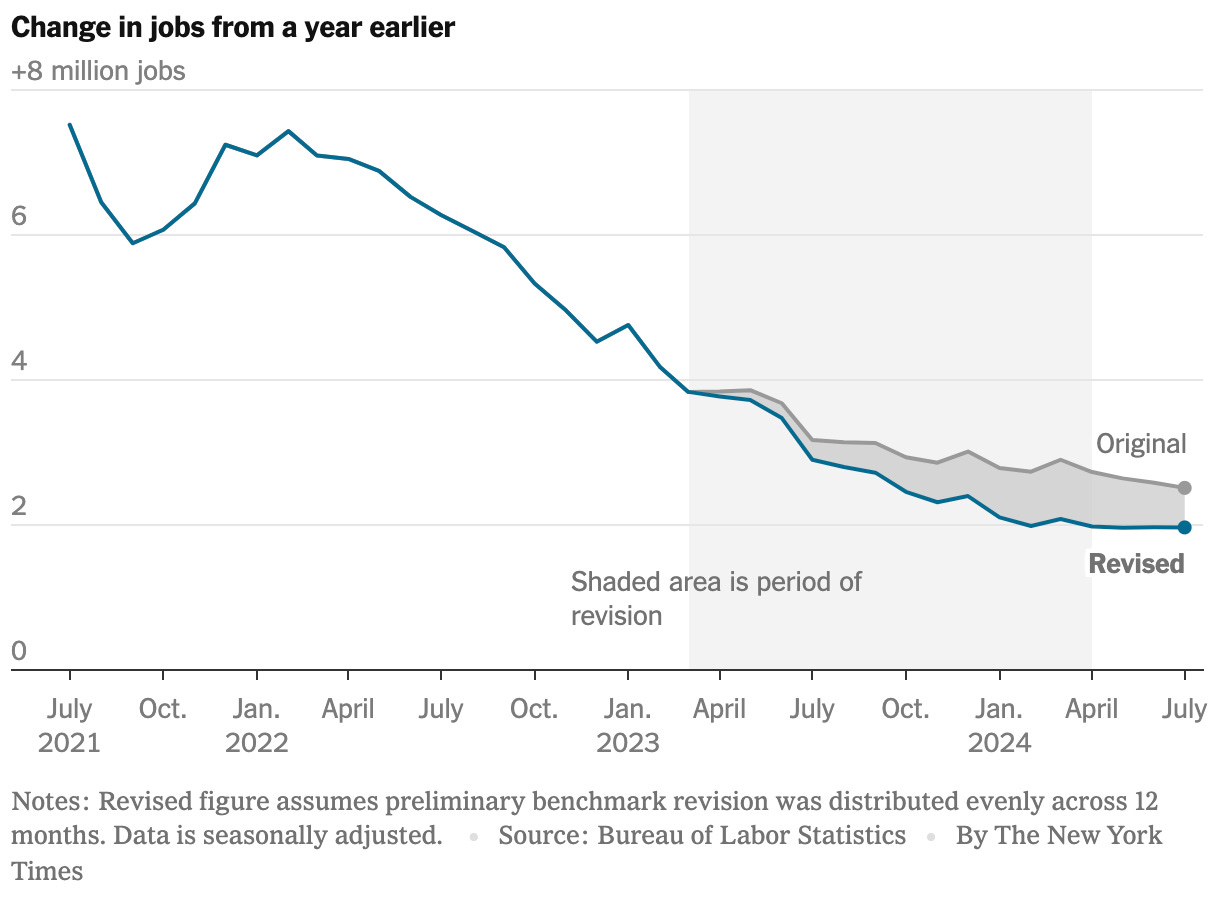

So, what is really going on in the economy right now? As we reported at the start of this month, some jobs numbers are hitting 2008-9 levels.

Typically, when jobless figures continue to rise, recessions follow because the unemployed and the workers who remain reduce spending habits and overall consumption in the economy.

So far, that scenario has not played out. But it also doesn’t mean the economy is doing well. This is why, in an election year, the White House will face questions raised by its rivals and from voters that will soon head to the ballot box.

Click here now to upgrade and become a Premium Prinsights reader!

Of course, incumbent politicians will want lower rates, which can spur growth and stoke borrowing. But the truth is that the economy takes considerable time to catch up to rate changes.

As the economy and the Fed navigate either a soft or hard landing, central bankers are altering other policies – ones that could impact the state of the financial system and beyond.

A Financial System Safeguard Gets Reduced

In many ways, the U.S. financial regulatory system is a pace setter for the world.

But, beyond the Fed, the Basel Committee on Banking Supervision (BCBS) created a set of capital requirements called the Basel III standards in response to the financial crisis.

Now, Fed officials want to loosen proposed capital requirements. That policy shift matters.

Once again, the Fed is putting Wall Street ahead of Main Street.

While the financial headlines were focused on the degree to which the Fed might cut rates, the Fed’s relaxed notion of standards will have a serious impact on the banking system over the long term. Simply put, megabanks will not need to adhere to a sufficiently high-degree of safeguards to cover their own risks.

Bloomberg reported that the Fed’s proposed revisions would nearly cut in half the 19% capital increase that regulators suggested for the eight biggest U.S. banks. Some of the same banks that got bailed out in 2008, including Citigroup Inc., Bank of America Corp. and JPMorgan Chase & Co., would face a 9% increase in the capital they must hold as a cushion against financial shocks instead.

That means the amount of money they are required to have on hand, should something go wrong, would be considerably less than what is proposed globally. If or, as history shows us, when Wall Street banks or their partners fail, they will once again turn to the government and taxpayer funds for an epic bailout.

As the non-profit, non-partisan, and independent organization Better Markets warned at the start of the year, “If Wall Street megabanks don’t have enough equity capital, then they either crash and throw Main Street Americans out of work and their homes like 2008 or trillions of dollars are used to bail out those megabanks as happened in 2008.”

The change to the so-called Basel III Endgame proposed rules could also signal a green light to other global central banks wanting to loosen their capital standards. Already, the Bank of England has cited “international competitiveness” as a reason to scale its rules back, too.

So, why does this matter now? Because at a time when political stakes are high, and the economy is sputtering – the Fed wants to give Wall Street a pass on banking safeguards.

The shortsightedness of the Fed being behind the curve to cut rates – and now setting itself up to be behind on key areas of economic and financial stability shows a dangerous pattern.

If the collapse of Silicon Valley Bank (SVB) last year showed us anything about the Fed’s inability to regulate the financial system, it’s that risks never truly go away. In fact, SVB’s inability to raise capital triggered its depositors to monitor how the bank was capitalized.

Last year, the Fed’s Vice Chair for Supervision, Michael Barr, stressed this concern, saying, “The risk of contagion implies that we need a greater degree of resilience for these firms than we previously thought, as the losses posed to society by the failure of a given firm are greater... The enhancements to the capital rules should improve the resilience of these firms.”

Yet, now he’s seemingly okay with Wall Street megabanks shying away from that same ethos.

Like the impact of rate cuts, only time will tell what’s to come.

For those looking for more stable outlets, gold can be a safe haven during financial turmoil.

On Wednesday, September 25th, we’ll be going live on Zoom with Rich Checkan and Adrian Day to discuss a range of topics – primarily focused on the precious metals space. In particular, we’ll cover topics spanning portfolio diversification, market outlooks and precious metals as a hedge to volatility. You can sign up to join the Zoom here.