The Silver Squeeze Just Got Real

China just posted its biggest silver grab in eight years. Here's why it matters as the country is tightening its grip on the world.

Silver is down roughly 35% from its January peak, even as the physical market tightens underneath it. There are plenty of macro explanations that have been offered for the pullback, from the war to inflation pressures, but none of them produce a single ounce of silver.

A temporary price correction isn’t a supply chain overhaul. That’s why we remain focused on entry opportunities during this correction period that reflect true long-term supply and demand factors.

China just posted its highest level of silver imports in eight years. The country imported more than 790 tons of silver from January and February, with February alone accounting for nearly 470 tons, a record for that month.

At the same time, Beijing is rolling out new export restrictions that limit refined silver shipments to a handful of state-approved firms holding special government licenses. That means two things are happening at once. The world’s largest buyer of silver is now buying more silver than ever, and the world’s largest processor of silver is making it harder for that metal to leave the country.

Where Silver Goes Now

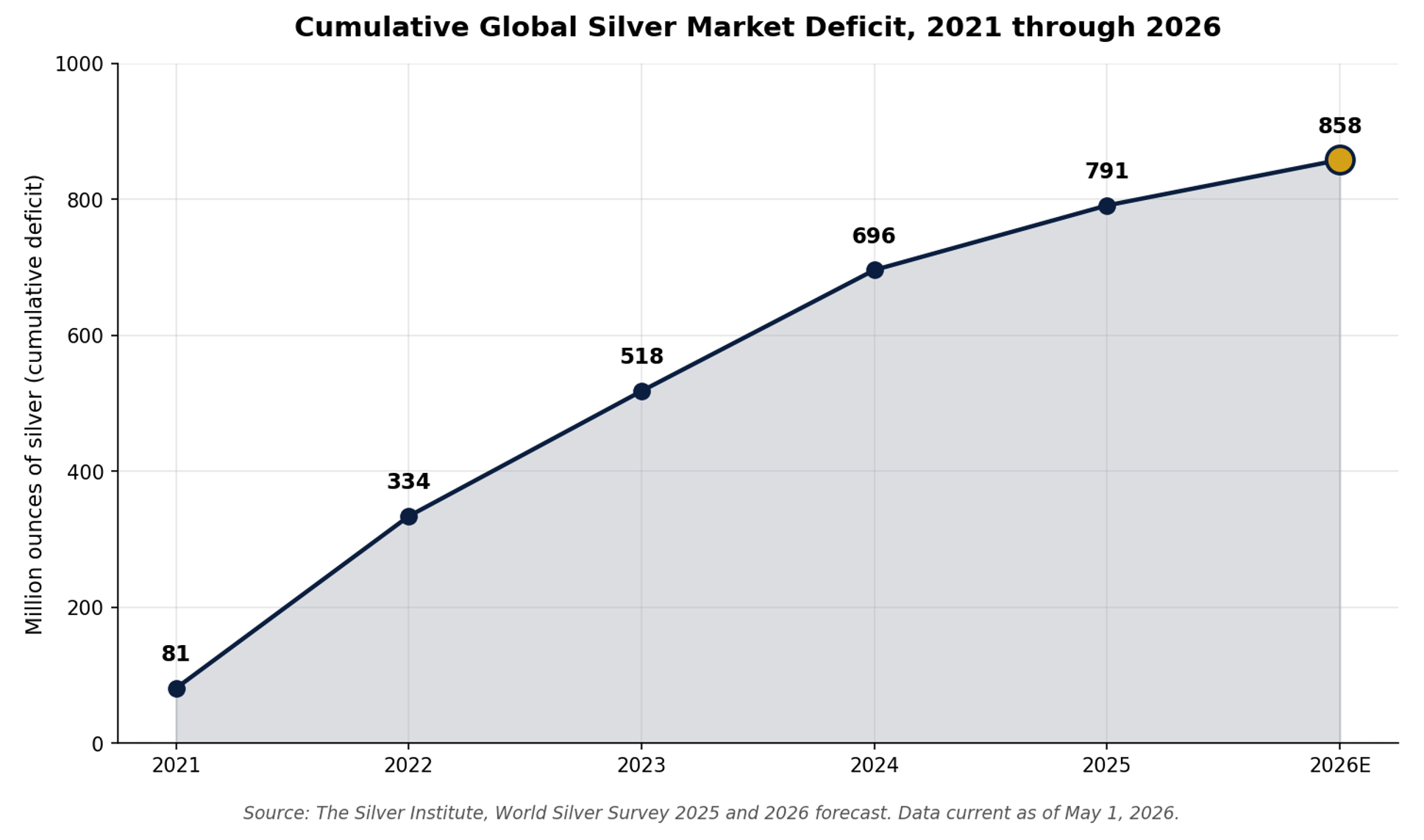

The Silver Institute is calling for a 67-million-ounce supply deficit in 2026, with some analysts putting the number well past 150 million ounces. The operating reality here is that no matter which figure you take, if it isn’t a surplus large enough to wipe out years of deficits, it’s still a supply scarcity signal.

Cumulative shortages since 2021 are already roughly 860 million ounces and growing.

Solar manufacturers remain the biggest industrial buyer of silver. Silver now represents 17-29% of the cost per watt of a photovoltaic module, up from around 10% in 2023. Meanwhile, EV production of 14-15 million units this year will consume about 12-15 million ounces.

Data centers, smart grid buildouts, and AI hardware needs are another large supply drag, and none of these industries or technology expansions are slowing down soon.

Why Supply Can’t Catch Up

Global mine production is projected at around 820 million ounces this year. Most of that silver comes up as a byproduct of copper, lead, and zinc mining. That means the new supply depends on whether copper and zinc producers want to expand.

As we detailed in our recent copper analysis, China announced on April 10 that it would halt sulfuric acid exports starting May 1. That restriction also tightens global silver supply, since most of the world’s silver comes up as a byproduct of the same copper, lead, and zinc operations that run on that acid.

Dedicated silver mines are rare, and many of the highest-grade deposits sit in remote, high-altitude terrain. Permitting, feasibility studies, construction, and ramp up periods can stretch close to a decade from discovery to first production.

This gap makes paper silver trading, the kind that moves off war and inflation headlines, a temporary substitute for real long-term value.

The gap is showing up right now in the flows. Since the Iran War began, the iShares Silver Trust (SLV) has been bleeding outflows while Sprott Physical Silver Trust (PSLV) and Aberdeen Physical Silver Shares (SIVR) have been pulling in capital. Investors are increasingly choosing funds with more direct physical backing over the paper proxies.

And there is a growing strain on the physical side, too. Registered silver on COMEX has dropped to 76 million ounces against 576 million ounces of open interest, which is coverage of 13.4%. That sits below the 15% level historically associated with delivery stress. Meanwhile Shanghai silver is now trading roughly 12-13% above LBMA spot and COMEX futures. The screen price has been falling through all of it.

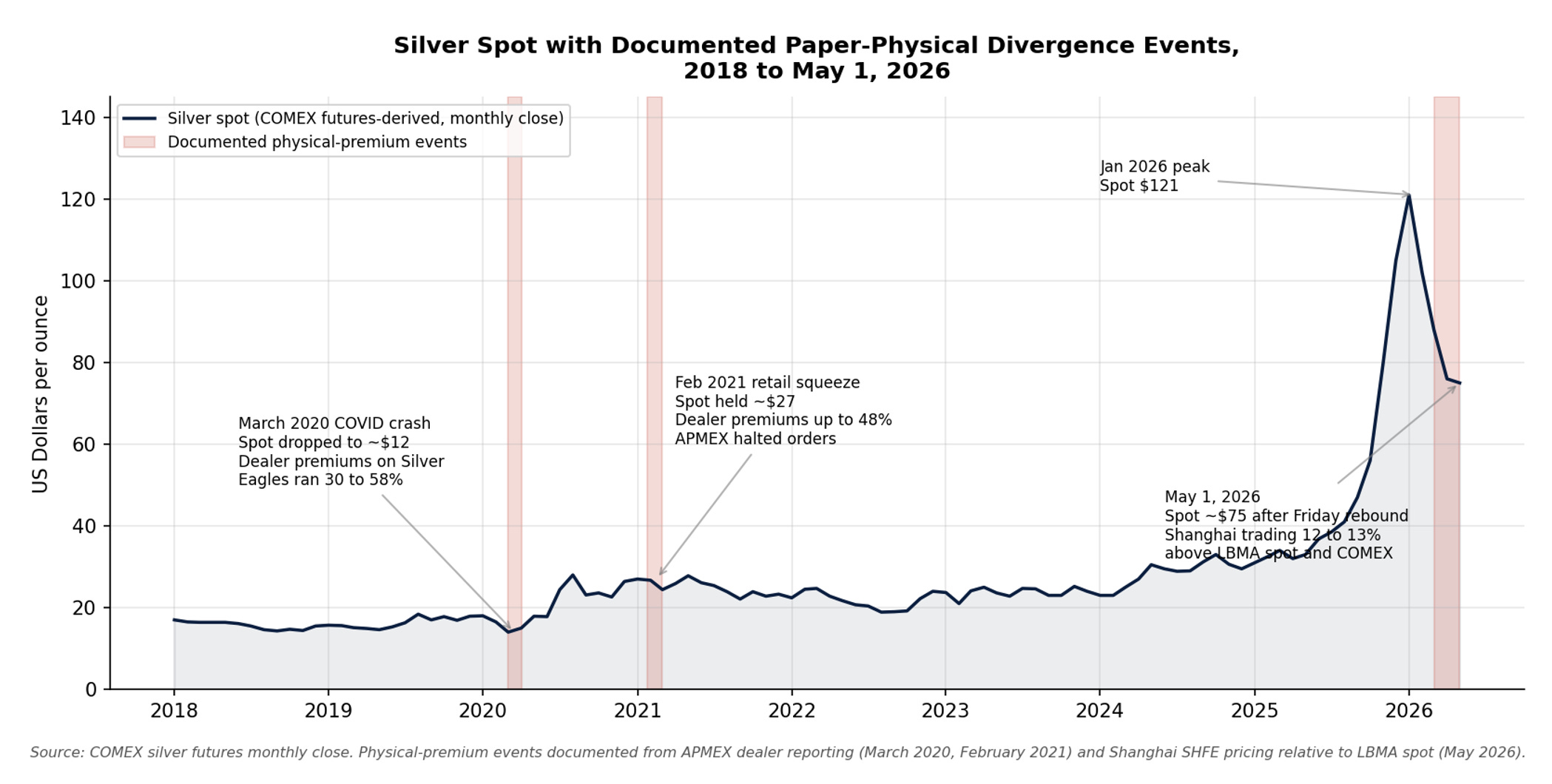

We have seen this gap that exists now between paper trading and physical silver production before. In 1980, the Hunt Brothers ran silver from $6 to almost $50 an ounce on futures buying. The COMEX changed the margin rules and the price collapsed to $11 in a single day. The amount of physical silver in the world barely changed across that move.

The same divergence showed up in March 2020 when paper silver crashed to around $12 while premiums on physical American Silver Eagles ran 30% or more over spot. Then, in early 2021, retail traders tried to squeeze the silver market on the back of the GameStop run, coordinating through Reddit’s #SilverSqueeze movement and pushing spot silver above $30 in a single session.

The paper price barely moved after that for weeks, while every major bullion dealer ran out of inventory and APMEX halted orders on a wide list of products.

What that looks like in practice is very different.

And I can tell you that when you stand at one of these sites and look around, scarcity becomes visceral. When you’re roughly 2,000 meters beneath the earth’s surface, it becomes unquestionable. You can see the scarcity of hard assets as you drive into their sites.

You can also see it in the single road that carries every ton of ore concentrate down the mountain, in the depth of the workings, and in the size of the ore body relative to the equipment and people around it.

Silver lies wherever geology put it, and the reality is that geology did not leave much of it in easy to access spots.

What This Means for Silver Investment

Physical silver keeps drawing from the safest haven locations as central banks and retail buyers shun paper alternatives that are demonstrably more volatile.

Producers with operating mines in stable jurisdictions are scarce. The management teams that actually run those mines well are scarcer still.

What all of this means is that six years of deficits have drawn down above ground inventories. China’s import numbers confirm what the inventory numbers already show. The world needs more silver than it has access to.

This is not a short-term trade driven by flashing headlines or fleeting market trends. What’s unfolding is a structural imbalance between physical supply and real demand – and it’s still building.

This analysis is not solely based on reports, I speak from physical experience! Only days ago, I went roughly 2,000 meters, or more than a mile, below the earth’s surface, Indiana Jones-style, to get to the bottom of silver scarcity and a budding supply jurisdiction. Not only does this process take time, but it requires highly-skilled professionals using increasingly complex methods to extract the metal and bring it to market as a refined product.

For Prinsights Pulse Premium and Founders+ readers, we will share a full report from that exact mine later this week with all the key details and everything you need to know. Our boots on the ground intel continues to give members not just an edge – but support for our model portfolios that are delivering real results.

Not a paid reader yet? Upgrade here now to unlock all Prinsights has to offer.